1 Chapter

Booming Construction Sector Driving Commercial AC Market Growth

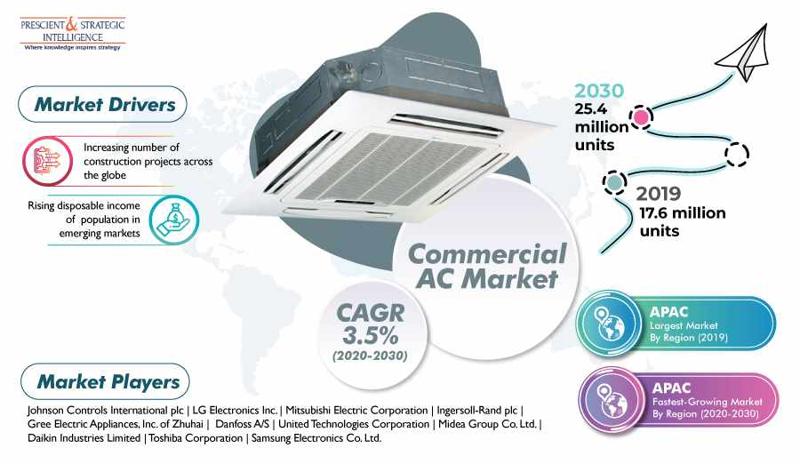

A number of factors such as the surging construction activities, owing to a massive rise in urban population and tourist activities, and soaring disposable income of the people in emerging economies are expected to drive the commercial air conditioner (AC) market at a CAGR of 3.5% during the forecast period (2020–2030). According P&S Intelligence, the market size is projected to increase from 17.6 million units in 2019 to 25.4 million units by 2030. One of the prominent growth drivers for the market is the expanding construction industry, primarily on account of rapid urbanization and a surge in tourist activities across the world. Moreover, the increasing government investments being made in the infrastructure sector will also boost the demand for commercial ACs in the coming years. Infrastructure units such as metro rail systems, airports, and office complexes require commercial ACs in abundance. For instance, the upcoming airports and metro stations in India and skyscrapers in the U.S. and the U.K. are generating a huge demand for these cooling systems. In recent years, the escalating use of low-global-warming-potential (GWP) refrigerants has become a major trend in the commercial AC market. At present, AC manufacturers use R22, R404A, and R507 refrigerants, which are based on chlorofluorocarbons (CFCs) and hydrochlorofluorocarbons (HCFCs), due to their easy availability. However, the soaring awareness about the adverse effects of such refrigerants has resulted in the large-scale adoption of R32 and other low-GWP variants across the world. At present, players of the commercial AC market, such as Johnson Controls International PLC, Mitsubishi Electric Corporation, Danfoss A/S, Samsung Electronics Co. Ltd., Midea Group Co. Ltd., United Technologies Corporation, and Toshiba Corporation, are focusing on introducing new cooling equipment to gain a competitive edge. For instance, in September 2019, Mitsubishi Electric Corporation launched a VRF system containing the R32 refrigerant in the U.K. to meet the burgeoning demand for environment-friendly electrical appliances. Similarly, in January 2020, LG Electronics Inc. introduced the Whisen ThinQ line of ACs in Seoul, South Korea. Categories under the type segment of the commercial AC market are variable refrigerant flow (VRF), ducted split/packaged unit, split units, chillers, and room ACs. In 2019, the split units category held the largest market share, as they can be used independently for effective and appropriate cooling. As compared to other AC types, these units are easy to maintain and operate. Whereas, the VRF category is expected to display the fastest growth during the forecast period, due to the high cost-effectiveness and energy efficiency offered by VRF systems. Geographically, Asia-Pacific (APAC) accounted for the largest share in the commercial AC market during the historical period (2014–2019), and it is also expected to demonstrate the fastest growth during the forecast period. This can be attributed to the growth of the construction sector in the region. Moreover, the booming population, especially in India and China, and mounting disposable income of people will also contribute to the market growth in the in the region in the foreseeable future. Thus, the flourishing construction industry, especially in developing countries, will steer the market growth in the forthcoming years. Source: P&S Intelligence

- Ongoing Story

Write a comment ...